The Software Continent

Decoding The Software Landscape by Ben Topor

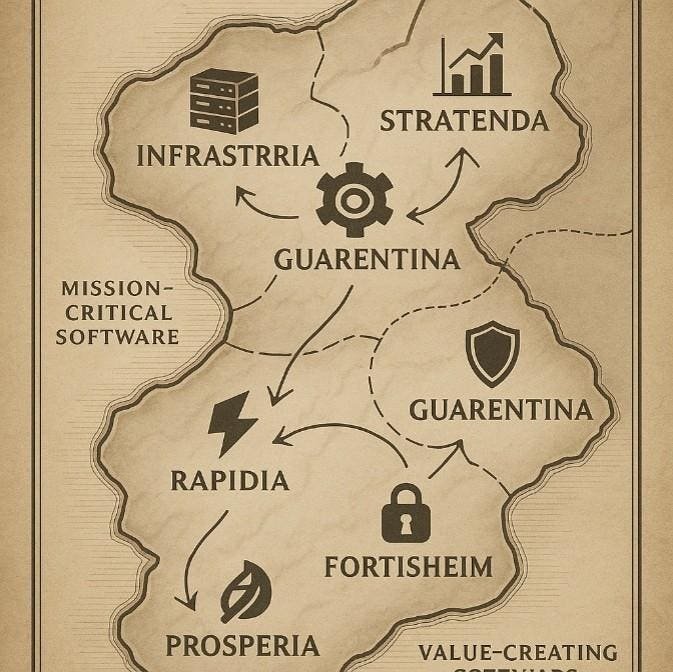

The eight city-states and how capital flows between them

The software industry is often described as constantly reinventing itself. Cloud, SaaS and now AI are each being framed as a reset. But beneath the surface, the structure of the industry is much more stable than it appears. What changes is not the ground, but the tools built upon it.

To understand how software markets are really behaving—especially in the current wave of AI-driven investment—it’s helpful to think of the industry not as a collection of categories, but as a continent. A system made up of distinct “city-states”, each governed by its own economic logic. Companies don’t just make products. operate in one of these cities, whether they realize it or not.

At the base of the continent are foundational systems—the level where software becomes part of the environment itself. Companies like Amazon Web Services or Snowflake are not chosen repeatedly. are integrated. Their success is not determined by features, but by necessity. Once embedded, they are extremely difficult to replace and over time, they quietly accumulate power.

Nearby are systems of record, the software that holds the “truth” within organizations. Salesforce in CRM or Workday in HR aren’t necessarily beloved products, but they are deeply established. Check the record and control the workflow. This creates a form of resilience that is less visible than growth, but much more enduring.

Another part of the continent is driven by an entirely different force: fear. In cybersecurity and compliance, spending isn’t about ambition, it’s about risk. Companies like CrowdStrike or Palo Alto Networks operate in an environment where the buyer is not asking how to improve results, but how to avoid failure. This is why, even in times of recession, these budgets tend to be maintained.

Further along the continent, the logic shifts from protection to optimization. There are some systems to reduce costs. Companies like UiPath or ServiceNow often enter organizations with a simple promise: eliminate inefficiencies. The value here is measurable, which makes adoption easier – but also makes the competition tougher. If a better or cheaper solution comes along, the change makes sense.

In contrast, another set of companies is focused on expanding revenue. Platforms like HubSpot or Shopify succeed when they can directly connect their product to development. This is a more ambitious category, but also a more fragile one. The central challenge is performance. If the product clearly generates revenue, it is necessary. If not, it’s one of the first tools to review.

Then there are systems built to inform decisions. Historically, this meant business intelligence tools like Tableau. Increasingly, in the age of artificial intelligence, it means something more ambitious: turning data into action. Companies like Databricks or Palantir are trying to bridge this gap. But as models and infrastructure become more commoditized, the real question is who owns the decision layer, not just the data.

A younger and faster growing part of the continent is defined by speed. Products like Notion or Canva succeed not because they are the most powerful, but because they deliver value almost immediately. In modern organizations, where patience for long implementations is low, time to value has become a competitive advantage in itself.

Finally, there are specialized systems built for specific industries. Companies like Veeva in life sciences or Procore in construction operate differently from horizontal software. They win not by being better across the board, but by being deeply aligned with the workflows of a single domain. Over time, these businesses often become highly defensible precisely because they are so customised.

Taken together, these eight city-states—foundations, systems of record, risk mitigation, cost reduction, revenue expansion, decision systems, velocity-based tools, and vertical solutions—form a cohesive structure. Each has its own rules and each rewards a different kind of company.

The mistake many operators make is to assume that these rules are interchangeable.

A product designed to increase revenue cannot be sold as a recording system. A cost reduction tool cannot rely on storytelling. he must constantly prove his worth. A vertical solution without real domain depth will struggle to gain trust. These are not execution failures – they are structural misalignments.

This framework also helps explain how capital moves today.

Despite the excitement surrounding artificial intelligence, capital does not flow evenly. It is concentrated in specific parts of the continent. The infrastructure and foundational layers—such as compute, data platforms, and model providers—have attracted massive investment because they are early adopters. At the same time, there is a surge of capital in applications that promise immediate results, particularly those that automate workflows rather than simply assist them.

Conversely, the more crowded horizontal categories are seeing increased pressure. As markets become saturated, capital begins to shift deeper—into vertical solutions where differentiation is harder to replicate and retention is stronger.

Seen through this lens, the current moment is not chaotic. It is redistribution.

For operators, the implication is simple. The most important strategic decision is not only what to build, but where you build it.

Each city rewards a different behavior. Each requires a different type of proof. And each offers a different path to resilience.

The companies that endure are not necessarily the most innovative. They are the ones who understand the rules of the city they are in – and fully align with them.

At Titan, this has become central to how opportunities are analyzed. Not asking if a company is “good”, but understanding where it is on the continent and how that position is evolving over time.

After all, the ground doesn’t change. But those who understand it can navigate it much more precisely.